Who Should Buy Long-Term Care Insurance? A Complete Guide (2025)

Long-term care insurance (LTCI) is designed to help cover the costs of extended care services for individuals who can no longer perform basic everyday tasks due to age, illness, or

Long-term care insurance (LTCI) is designed to help cover the costs of extended care services for individuals who can no longer perform basic everyday tasks due to age, illness, or disability. But is long-term care insurance worth it? With rising healthcare costs and an aging population, understanding who should buy long-term care insurance, when to buy it, and how to choose the right policy is essential. This guide will help you navigate these decisions with clarity, offering a step-by-step framework, cost comparisons, and real-world insights to ensure you make the best choice for your future.

What Is Long-Term Care Insurance?

Long-term care insurance is designed to cover the costs of extended care services, such as nursing home care, assisted living, or in-home care, which are not typically covered by health insurance or Medicare. It provides financial protection against the high expenses associated with chronic illnesses, disabilities, or age-related conditions.

Is long-term care insurance worth it?

It can be, especially if you want to avoid the financial burden of paying for extended care out-of-pocket. However, it depends on your health, finances, and family history.

Flexibility in Care Options: Covers various services like home care, assisted living, or nursing homes.

Reduced Family Burden: Eases financial and caregiving stress on loved on

Why Do People Buy Long-Term Care Insurance?

People purchase LTC insurance to protect their savings and assets from being depleted by long-term care costs. It also provides peace of mind, ensuring that they can access quality care without burdening their families financially.

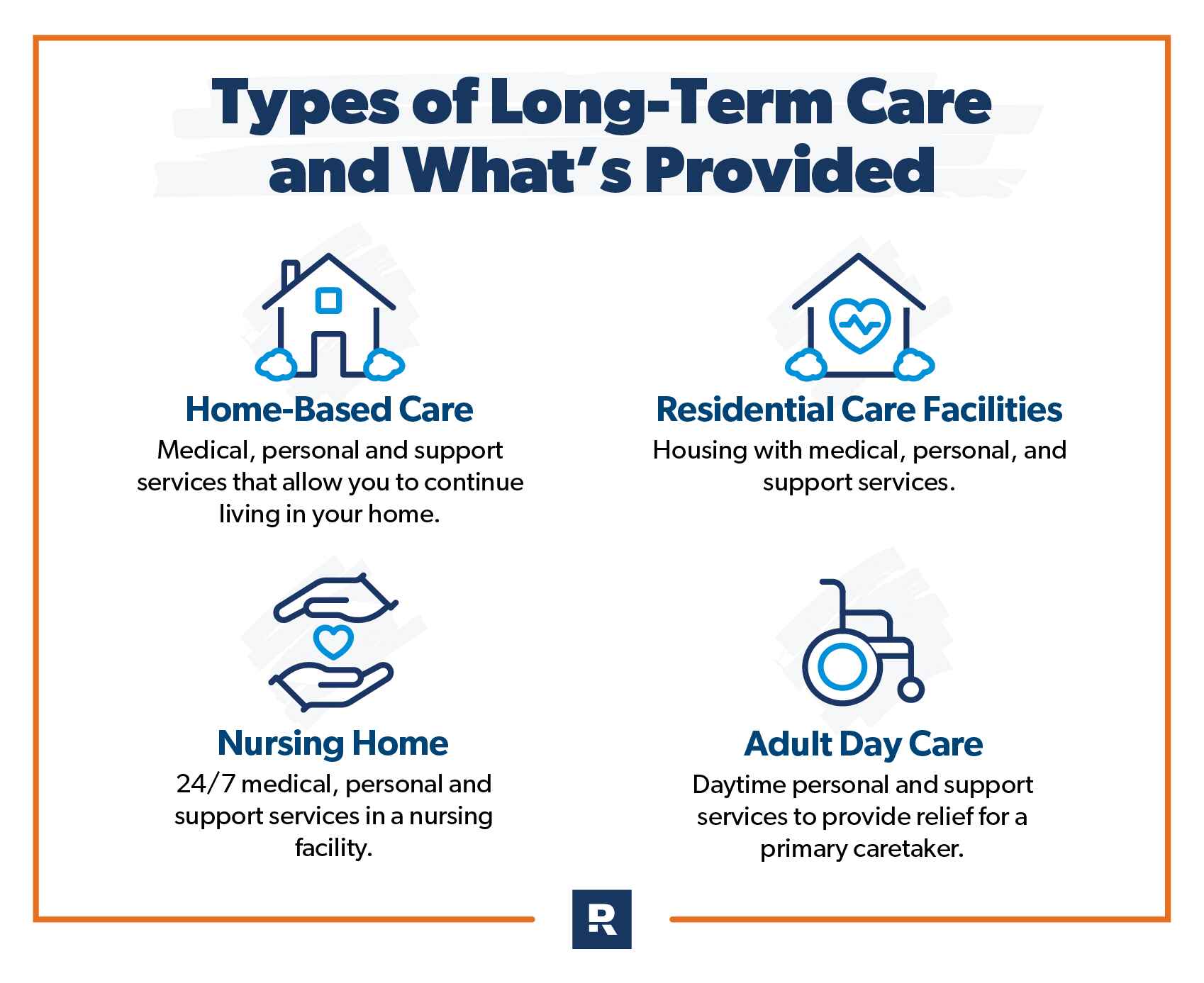

What Does It Cover & What Doesn’t It Cover?

Long-term care insurance typically covers the following services:

Nursing home care

Assisted living care

Home health care

Hospice care

However, it does not cover:

Care from family members

Medical care or treatments (which are covered by other insurance plans)

Inpatient hospital care or emergency services

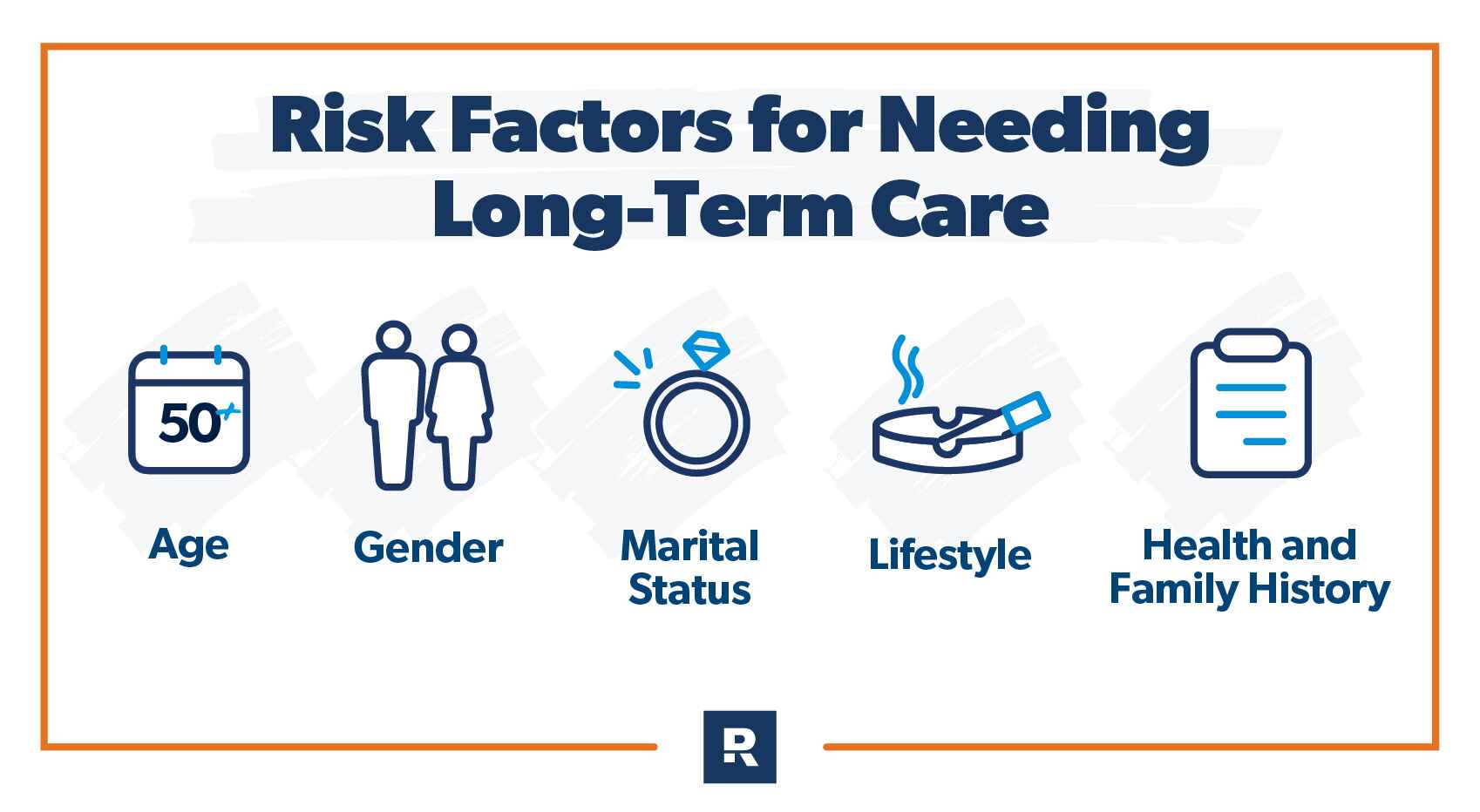

Who Really Needs Long-Term Care Insurance?

The decision to buy LTC insurance depends on several factors, including your age, health, and family history. Here's a breakdown of who could benefit from this type of policy.

Should You Buy It in Your 40s, 50s, or 60s?

The best time to buy long-term care insurance is typically in your 50s, when you're still in good health and can lock in lower premiums. Waiting until your 60s or later can lead to higher premiums or even rejection due to pre-existing health conditions.

How Family Medical History Affects Your Decision

Your family medical history plays a critical role in your decision to buy LTC insurance. If there’s a history of chronic illness or conditions like Alzheimer’s, you may be at a higher risk of needing long-term care. This increases the likelihood of needing LTC insurance.

Who Can Skip Long-Term Care Insurance?

If you have significant assets or are financially able to self-pay for long-term care, LTC insurance may not be necessary. Additionally, younger individuals who do not have a family history of debilitating diseases might consider skipping this insurance.

Best Time to Buy Long-Term Care Insurance

When should you purchase long-term care insurance? Timing is crucial to avoid paying inflated premiums or being denied coverage.

At What Age Should You Get a Policy?

Generally, the earlier you purchase long-term care insurance, the more affordable it will be. Consider buying it in your 40s or 50s to get the best rate. At this stage, you’re likely still healthy enough to qualify, and premiums will be lower compared to waiting until your 60s or beyond.

How Health Status Affects Your Premiums?

Your health status is one of the most significant factors that determine your long-term care insurance premiums. Those in good health will pay less, while individuals with chronic conditions or a history of medical problems will face higher premiums.

Mistakes People Make When Buying Too Late

Buying long-term care insurance too late can lead to higher premiums, exclusions based on pre-existing conditions, or even being denied coverage altogether. Start planning early to avoid these pitfalls.

How to Choose the Right Long-Term Care Insurance Policy?

When purchasing long-term care insurance, it’s important to choose a policy that meets your needs. Here are some key factors to consider.

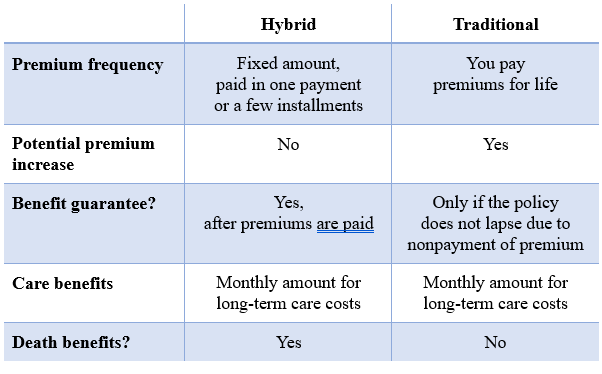

Traditional vs. Hybrid Policies – Which One Is Better?

Traditional long-term care insurance typically offers pure coverage for long-term care, while hybrid long-term care policies combine life insurance or annuities with long-term care benefits. Hybrid policies might be a better choice for those who want to ensure their beneficiaries receive a payout if they don’t need care.

Key Features to Look for in a Policy

Key features to consider include:

Daily benefit amount

Benefit period (how long the policy will pay for care)

Waiting period before benefits kick in

Network of care providers

Inflation protection

How Much Does Long-Term Care Insurance Cost?

The cost of long-term care insurance varies based on factors like age, health, and the level of coverage chosen. Below are some considerations.

What Factors Affect the Price?

Age at the time of purchase

Health status and medical history

Coverage amount and policy type (traditional vs. hybrid)

Optional riders (inflation protection, etc.)

Is It Worth It Compared to Self-Paying?

While LTC insurance premiums can be costly, the alternative—self-paying for long-term care—can be financially devastating. Nursing home care costs can exceed $100,000 per year in many areas, making insurance a worthwhile investment for most individuals.

Cost Comparison Table

Option

Annual Cost

Pros

Cons

LTC Insurance

2,000−2,000−4,000

Protects savings, predictable costs

Premiums can increase over time

Self-Paying (Nursing Home)

$100,000+

No upfront premiums

Can deplete savings quickly

Medicaid

Varies

Covers low-income individuals

Requires asset depletion, limited choices

Alternatives to Buying Insurance

Alternatives include Medicaid, personal savings, or even family care. However, Medicaid typically requires that you exhaust most of your savings before qualifying, and it may not cover all the services you need.

Common Myths About Long-Term Care Insurance

There are several misconceptions about long-term care insurance that could lead to poor decision-making.

“I Can Rely on Medicare” and Other Misconceptions

Many people believe Medicare covers long-term care, but it only covers short-term skilled nursing care. LTC insurance fills this gap, more flexible, providing coverage for extended care needs.

Why Not Everyone Needs LTC Insurance

Not everyone needs LTC insurance, especially if they have substantial savings or other resources to cover long-term care costs. Assess your financial situation carefully before deciding whether this insurance is right for you.

Final Decision – Should You Buy Long-Term Care Insurance?

Ultimately, the decision to purchase long-term care insurance depends on your personal circumstances.

You should consider buying LTC insurance if:

You are in your 40s or 50s

You have a family history of chronic illnesses

You want to avoid the financial burden of long-term care

You don’t have sufficient savings to cover care costs

Who Can Consider Other Options?

High-net-worth individuals who can self-insure

Those who qualify for Medicaid

People with strong family support systems

Best Next Steps for Making a Decision

Assess your financial situation and health history

Compare policies and get quotes from multiple providers