What Is IUL Insurance? A Simple Guide to Indexed Universal Life

- Home

- What Is IUL Insurance? A Simple Guide to Indexed Universal Life

What Is IUL Insurance? A Simple Guide to Indexed Universal Life

Indexed Universal Life Insurance

Indexed Universal Life insurance, often called IUL, is a form of permanent life insurance designed to last your entire lifetime. Along with a death benefit, it includes a cash value feature that can grow over time.

Because of this structure, IUL appeals to individuals who want lifelong coverage while also seeking the potential for higher returns compared to standard universal life policies. It blends protection with the opportunity for tax-advantaged cash value growth.

In this guide, we’ll walk through how Indexed Universal Life works, its key features, and whether it aligns with your long-term financial objectives.

Key Takeaways

Indexed universal life insurance is a permanent life insurance option that provides lifetime coverage along with the potential to build cash value tied to a market index.

The cash value is not directly invested in the stock market. Growth is influenced by index performance and limited by factors like caps, floors, and policy charges, which can impact overall returns.

These policies offer flexibility in premiums and death benefits, but they are not set-and-forget products. Regular review is important to make sure the policy stays adequately funded.

IUL insurance can be a good choice for people who want long-term protection with growth potential, but it is not suitable for every financial situation or goal.

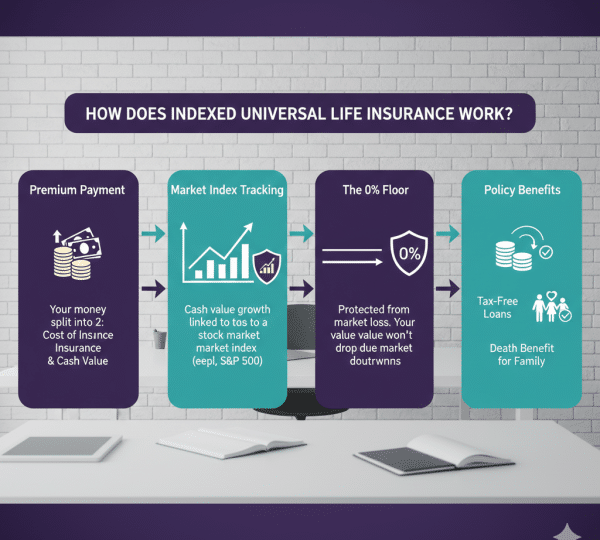

How Does IUL Insurance Work?

Indexed universal life insurance combines lifetime coverage with a cash value feature that has the potential to earn interest over time. It offers more flexibility than term or whole life insurance, but that flexibility also means there are several factors that influence how the policy performs in the long run.

An IUL policy is built around two core components. The first is the death benefit, which provides financial protection to your beneficiaries. The second is the cash value account, which can accumulate value based on interest credited according to a selected market index.

These two elements work together. The way premiums are allocated, the cost of insurance, and the credited interest all play a role in how the policy grows and how sustainable it remains over time.

Death Benefit Flexibility

The death benefit is the payout your beneficiaries receive if you pass away while the policy is active. IUL policies are built to provide lifetime protection, but that protection depends on keeping the policy adequately funded over time.

Based on how the policy is structured, the death benefit can either stay level or increase as the cash value grows. Some policies also allow you to adjust the death benefit later if your financial situation changes. Any changes are subject to underwriting guidelines and minimum funding rules.

Cash Value Growth

Every IUL policy includes a cash value account. When you pay your premium, part of it goes toward the cost of insurance and policy expenses. The remaining portion is allocated to the cash value, where it has the potential to grow.

Growth is not guaranteed. It depends on several factors, including policy fees, the amount of premium paid, and how interest is credited. If the cash value does not grow enough to cover rising insurance costs and charges, you may need to contribute additional premiums to keep the policy in force. Even with protective features, cash value can decrease over time, especially if the policy is underfunded.

Many IUL policies offer different allocation options. In addition to indexed accounts, some insurers provide a fixed account that earns a steady interest rate. You can split your cash value between these options to balance stability and growth potential.

Index-Linked Crediting

In an IUL policy, interest is credited based on the performance of a market index, such as the S&P 500, the Dow Jones Industrial Average, or the Nasdaq Composite. Your cash value is not directly invested in these markets. Instead, the insurer uses a formula to determine how much interest is credited.

Most index strategies include:

A cap, which sets the maximum interest you can earn during strong market years.

A floor, often 0 percent, which helps protect against losses caused solely by negative index performance.

A participation rate, which determines how much of the index’s gain is applied to your policy.

These features help reduce downside risk, but they also limit how much you can earn. Actual results depend on index performance, the policy’s design, and ongoing charges that may reduce net growth.

Example: How an IUL Policy Might Work Over Time

Tony and Danielle are in their mid-40s with two teenage children. Tony is self-employed, and his income varies from year to year. Danielle works as a nurse, providing a steady income for the household. They are financially stable but want another tax-advantaged way to build savings.

Tony purchases an IUL policy and pays $400 per month in premiums. Around $200 covers the cost of insurance and policy expenses, while the remaining $200 goes into the cash value account. He decides to allocate 75 percent, or $150 per month, to the indexed account and 25 percent, or $50 per month, to the fixed account. Over time, the performance of the index, combined with policy charges and allocation choices, will determine how the cash value grows and ultimately how the policy performs.

Indexed Universal Life (IUL) Insurance: Pros and Cons

Pros of IUL | Cons of IUL |

Lifetime coverage – Provides permanent protection as long as the policy stays funded. | Complex structure – Harder to understand than term or traditional whole life policies. |

Cash value growth potential – Earnings are linked to a market index, offering higher upside than fixed interest policies. | Capped returns – Growth is limited by participation rates and caps, so you don’t receive full market gains. |

Downside protection – Most policies include a 0% floor, protecting against market losses in negative years. | Policy fees and charges – Insurance costs, admin fees, and riders reduce overall cash value growth. |

Flexible premiums – Ability to adjust payments within policy limits. | Risk of lapse – Underfunding or poor performance may cause the policy to lapse. |

Adjustable death benefit – In many cases, you can modify the death benefit as needs change. | Requires active monitoring – Needs regular review to ensure proper funding and performance. |

Tax advantages – Cash value grows tax-deferred; policy loans may be tax-free if structured properly. | Not ideal for short-term goals – Designed for long-term financial planning, not quick returns. |

Why People Choose IUL?

Lifetime protection

IUL is a permanent life insurance policy. As long as it remains properly funded, it provides a death benefit that lasts your entire life, not just a fixed term.

Opportunity for higher cash value growth

Instead of earning a fixed interest rate, the cash value is tied to the performance of a market index. This structure gives you the potential to earn more than traditional fixed universal life policies in strong market years.

Protection during market downturns

Most IUL policies include a minimum guaranteed interest rate, often 0 percent. That means if the market performs poorly, your cash value is typically protected from negative returns.

Premium and benefit flexibility

You usually have the option to adjust premium payments within policy limits. Some policies also allow changes to the death benefit and the addition of riders to fit changing financial goals.

Tax benefits The cash value grows on a tax deferred basis. In many cases, policy loans can be accessed without immediate taxes, provided the policy is structured and managed correctly.

Things to Consider Before Buying

More complex than other policies

IUL policies are not as straightforward as term life or traditional whole life insurance. Understanding how caps, participation rates, and policy charges work is essential.

Fees can impact performance

Insurance costs, administrative fees, and optional rider charges are deducted from the policy. These expenses can reduce the overall growth of your cash value.

Limited upside in strong markets

Even if the linked index performs very well, your returns are usually subject to caps and participation rates. This means you do not receive the full market gain.

Possibility of policy lapse

If premiums are too low or the policy underperforms for an extended period, the cash value may not be enough to cover internal costs. In that case, the policy could lapse without additional funding.

Better suited for long term goals

IUL is generally not designed for short-term financial needs. It works best for individuals who are planning decades ahead, such as for retirement income or legacy planning.

IUL is generally not designed for short-term financial needs. It works best for individuals who are planning decades ahead, such as for retirement income or legacy planning.

IUL vs Whole Life Insurance

Indexed Universal Life (IUL) insurance vs whole life insurance both fall under permanent life coverage, meaning they are designed to last your entire lifetime. That said, the way they function and the type of policyholder they suit can be quite different.

Whole life insurance is built around stability. Premiums stay the same, the death benefit is guaranteed, and the cash value grows at a steady, predetermined rate. It’s often chosen by people who value certainty and prefer a policy that runs with minimal involvement.

IUL insurance, on the other hand, focuses on flexibility and growth potential. Premiums can be adjusted within limits, and the cash value has the opportunity to grow based on the performance of a market index rather than a fixed rate. This creates the possibility of higher returns over time, but it also introduces variability. Growth is not guaranteed, policy charges may be higher, and the policy typically needs regular monitoring to make sure it remains properly funded.

In simple terms, whole life favors predictability and simplicity, while IUL appeals to those who are comfortable with a more hands-on approach in exchange for greater long term upside.

Alternatives to Indexed Universal Life Insurance (IUL)

Indexed Universal Life (IUL) insurance combines lifelong coverage with cash value growth tied to a stock market index. While it can be a flexible option for some individuals, it isn’t the right fit for everyone.

If your goals are protection, predictable growth, or retirement planning, several alternatives may better match your needs.

Below are the most common and practical alternatives to IUL — and who they’re best suited for.

1. Term Life Insurance – Best for Pure Protection

If your primary goal is to protect your family financially, term life insurance is often the most affordable and straightforward option.

How it works:

Coverage lasts for a fixed period (10, 20, or 30 years)

No cash value component

Lower premiums compared to permanent policies

Who it’s best for:

Young families

Homeowners with a mortgage

Income earners needing temporary coverage

Unlike IUL, term life focuses entirely on protection making it ideal for families in Florida or across the U.S. who want maximum coverage at minimal cost.

2. Whole Life Insurance – Guaranteed Stability

Whole life insurance provides permanent coverage with guaranteed cash value growth and fixed premiums.

Key advantages:

Lifetime protection

Guaranteed interest growth

Predictable premium payments

Potential dividends (with participating policies)

Important to know:

You don’t control how the cash value is invested—the insurance company manages it. While growth is typically slower than market-based policies, it’s more stable.

This option may appeal to conservative planners who value certainty over market-linked returns.

3. Fixed Universal Life (FUL) – Conservative Flexibility

Fixed Universal Life is a type of universal life insurance that credits a declared interest rate set by the insurer.

Benefits:

Permanent coverage

Flexible premiums (within limits)

Steady, predictable interest growth

Drawbacks:

Growth potential is typically lower than IUL or VUL

Returns are not tied to stock market performance

If you want flexibility but prefer to avoid market exposure, this can be a middle-ground option.

4. Variable Universal Life (VUL) – Higher Growth, Higher Risk

Variable Universal Life (VUL) combines permanent life insurance with investment sub-accounts similar to mutual funds.

Pros:

Greater growth potential

Investment flexibility

Lifetime coverage

Cons:

Market risk exposure

Requires active management

Cash value can decline in down markets

VUL may be appropriate for experienced investors comfortable with volatility and long-term market swings.

5. Tax-Advantaged Retirement Accounts – Often a Smarter First Step

Before using life insurance as an investment tool, many financial professionals recommend maximizing:

401(k) plans (especially if employer matching is offered)

Traditional or Roth IRA accounts

SEP-IRA (for self-employed individuals)

Why?

Lower fees

Transparent investment options

Clear tax advantages

No insurance cost drag

For many households in Florida and nationwide, fully funding retirement accounts first may be more efficient than relying on IUL for wealth accumulation.

How to Decide Which Option Is Right for You?

Choosing between IUL and its alternatives depends on:

Your risk tolerance

Income level

Retirement timeline

Need for guaranteed growth

Desire for flexibility

Estate planning goals

No single policy works for everyone.

For some, IUL provides a balance between protection and growth. For others, term insurance combined with retirement investing may be a more cost-effective strategy.

Speaking with a licensed insurance professional can help you compare illustrations, understand policy costs, and choose coverage aligned with your financial goals.

Frequently Asked Questions

1. What is Indexed Universal Life (IUL) insurance?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that provides lifelong coverage while allowing your cash value to grow based on the performance of a market index, such as the S&P 500. It combines a death benefit with tax-advantaged cash value accumulation.

2. Is IUL insurance a good investment?

IUL is primarily life insurance, not a pure investment. However, it can be a powerful financial tool for tax-deferred growth, retirement income planning, estate planning, and wealth transfer when structured properly.

3. Can I lose money in an IUL policy?

Your principal is generally protected from market losses due to the floor rate (often 0%). However, policy fees, charges, or poor funding strategies can reduce your cash value if not managed correctly.

4. How is IUL different from term life insurance?

Term life insurance provides coverage for a specific period (10, 20, or 30 years) and does not build cash value. IUL provides lifelong coverage and includes a cash value component that can grow over time.

4. Is Indexed Universal Life insurance tax-free?

The death benefit is generally income-tax-free to beneficiaries. Cash value grows tax-deferred, and policy loans are typically tax-free if the policy remains in force and is structured properly.

5. Who should consider an IUL policy?

IUL may be suitable for:

High-income earners looking for tax-advantaged growth

Business owners

Individuals maxing out 401(k) or IRA contributions

Families wanting lifelong coverage with wealth-building potential

6. How long does it take for an IUL to build cash value?

Cash value typically takes several years to accumulate significantly. IUL is designed as a long-term strategy, often 10–15+ years for optimal performance.

7. Can I adjust my premiums in an IUL policy?

Yes. One of the key benefits of IUL is flexible premiums. You can increase or decrease payments (within limits) as long as there’s enough cash value to cover policy costs.

8. What happens if the market crashes?

If the index performs negatively, your policy is protected by the floor rate (commonly 0%), so you won’t lose credited interest for that period. However, insurance costs still apply.

9. Is IUL better than a 401(k)?

They serve different purposes. A 401(k) is a retirement investment account, while IUL is life insurance with tax-advantaged growth. Many people use both as part of a diversified financial strategy.